Virtual dollar cards: how to get them online and pay worldwide

Not long ago, it seemed natural to pick a single card and use it for everything: shopping, subscriptions, travel. Convenient, simple, familiar. But today, relying on only one payment method actually limits flexibility instead of enhancing it. In the past, people used a single card simply because there weren’t other options.

In 2025, there’s no need to stick to just one card. Even one virtual card is often not enough. It’s better to use multiple cards for different purposes. And issuing any virtual card online takes just a few minutes, they work globally as long as they’re Visa or Mastercard.

In 2025, there’s no need to stick to just one card. Even one virtual card is often not enough. It’s better to use multiple cards for different purposes. And issuing any virtual card online takes just a few minutes, they work globally as long as they’re Visa or Mastercard.

Why a virtual dollar card isn’t a cure-all

We tend to value simplicity. One card seems logical — fewer passwords, fewer apps, less confusion.

The paradox is that even experienced users often issue a single dollar card thinking it will solve everything. But when they encounter foreign advertising platforms, spending limits, or currency fees, it becomes clear: there’s no universal solution. Payment systems classify transactions differently, and what works for one platform may not work for another.

This is why having a set of cards from different providers is the only practical strategy. Even then, you need to test tools, manage risk, and monitor fees.

Fintech platforms no longer focus on a single product, they build entire ecosystems for various payments. Users can issue a card for a specific purpose, set a limit, choose a currency, and delete it when it’s no longer needed. It’s a flexible system where the principle is “one tool per task.”

This gives rise to personal payment setups: one card for travel, another for online shopping, and a third for business payments. Each is secure, independent, and works within its intended scenario.

Fintech in 2025: using it to the fullest

Task-specific cards make spending transparent. Instead of trying to remember where money went, you can simply check which card was used. Security is higher: if suspicious activity occurs, you can block one card without affecting the others. Dollar cards also reduce currency losses, avoiding cross-rate fees and unexpected charges during international payments.

There’s also a psychological benefit. Having several simple tools gives a sense of stability. You don’t rely on a single card that a bank or payment processor could block. Everything can be duplicated, controlled, and planned.

Creating virtual cards only requires internet access. Users select a platform, FinTech provider or neobank, complete a short verification, fund the account, and receive the card details. The card is immediately active and ready for payments worldwide.

Modern platforms let users issue multiple cards from one interface, adjust limits, change currencies, and set expiration dates. Users control how each card is used.

It’s now possible to issue a card in just a couple of minutes.

-

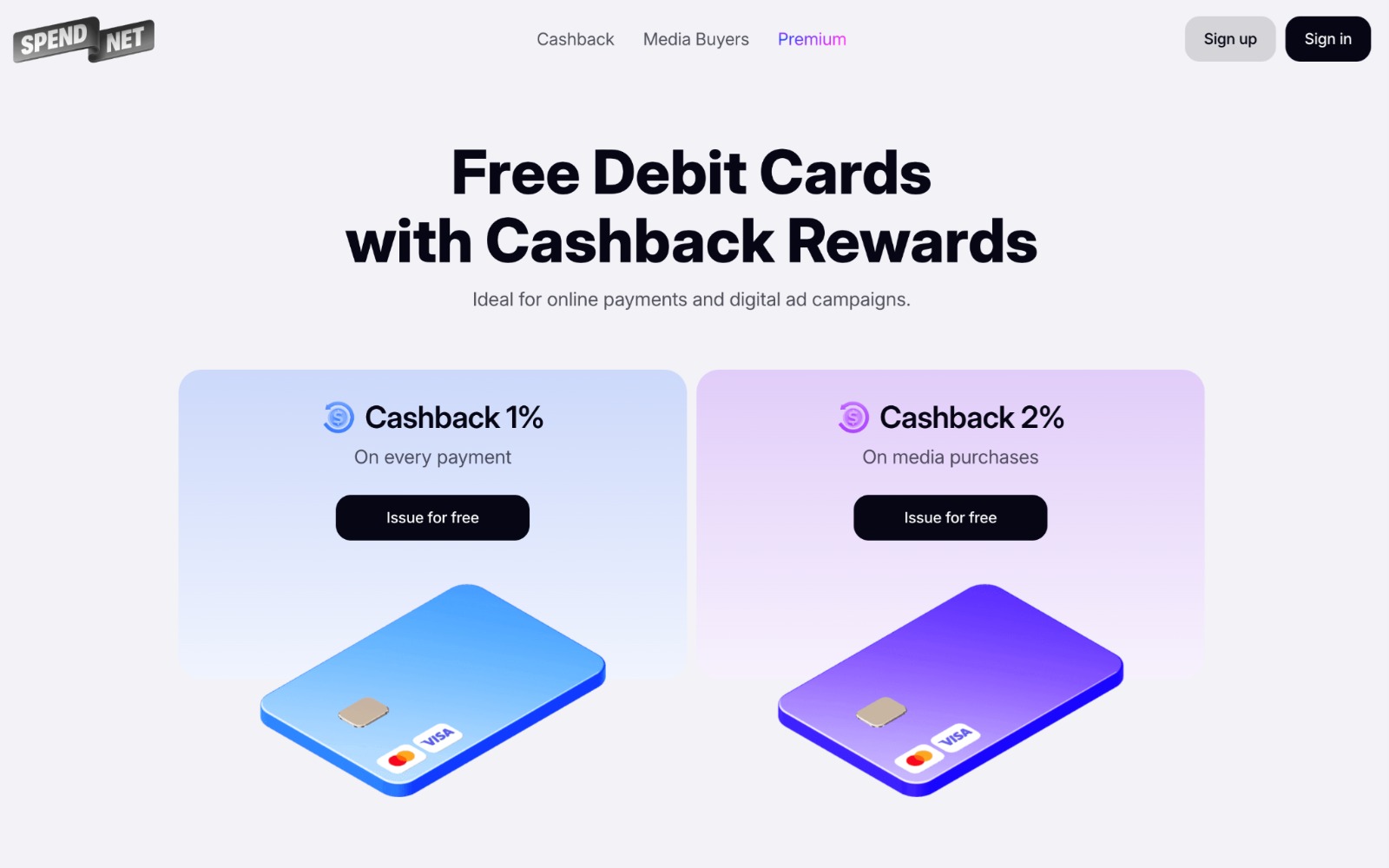

Spend.net

One prominent provider is Spend.net, which makes virtual cards highly accessible. There are no issuance or maintenance fees, and the cards work globally on Visa and Mastercard networks.

Essentially, users get a full-featured payment tool for any purchase from online stores to ad accounts. All virtual dollar payment cards are accepted worldwide, and anyone can issue them.

Spend.net also offers a unique feature: each purchase returns 1% cashback directly to the balance. Frequent dollar spenders can turn even small purchases into tangible benefits. Top-ups are possible via cryptocurrency, with fees usually under 2%, while all other operations — transactions, currency conversions, and refunds are free. Registration takes just a few minutes, and security is ensured with 3D Secure.

Spend.net also offers a unique feature: each purchase returns 1% cashback directly to the balance. Frequent dollar spenders can turn even small purchases into tangible benefits. Top-ups are possible via cryptocurrency, with fees usually under 2%, while all other operations — transactions, currency conversions, and refunds are free. Registration takes just a few minutes, and security is ensured with 3D Secure.

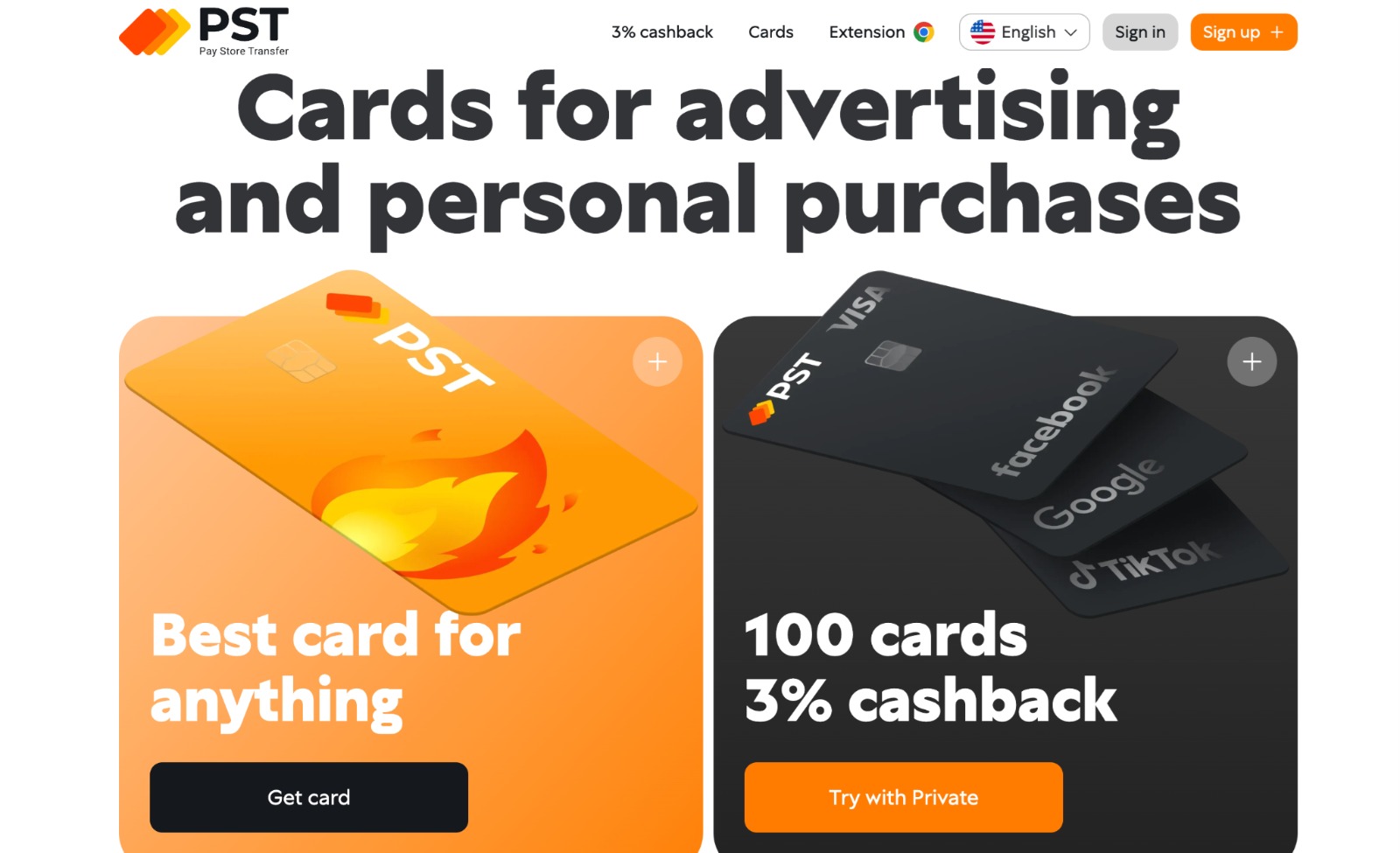

2. PSTNET

Another strong player is PSTNET, a highly technological fintech provider. The platform focuses on users who value flexibility and speed for international payments.

Their cards are popular among travelers and entrepreneurs paying for ads or booking flights abroad. PSTNET cards have no top-up or spending limits, and funding fees are just 2%.

New users get a bonus – the first USDT deposit is fee-free.

The platform supports 18 cryptocurrencies, automatically converting them to dollars, and account management is available via a convenient browser extension or mobile app. Security is built to banking standards, with two-factor authentication and 3D Secure protecting every operation. Registration is simple, with login options through Google, Apple ID, or even Telegram. Once funded, the card is active immediately.

The platform supports 18 cryptocurrencies, automatically converting them to dollars, and account management is available via a convenient browser extension or mobile app. Security is built to banking standards, with two-factor authentication and 3D Secure protecting every operation. Registration is simple, with login options through Google, Apple ID, or even Telegram. Once funded, the card is active immediately.

3. Ezzocard

For users who value anonymity and simplicity, Ezzocard is ideal. It doesn’t require traditional accounts or identity checks. Users simply select a card on the website, pay for it, and instantly receive the details. Each card is single-use, with a fixed denomination—ranging from $10 to $2,000.

These cards cannot be refilled, which makes them secure: no data is stored, minimizing hacking risks. They’re perfect for one-off transactions such as purchases on foreign websites or subscription payments. Once used, the card is deleted, leaving the user with a clean financial history.

These cards cannot be refilled, which makes them secure: no data is stored, minimizing hacking risks. They’re perfect for one-off transactions such as purchases on foreign websites or subscription payments. Once used, the card is deleted, leaving the user with a clean financial history.

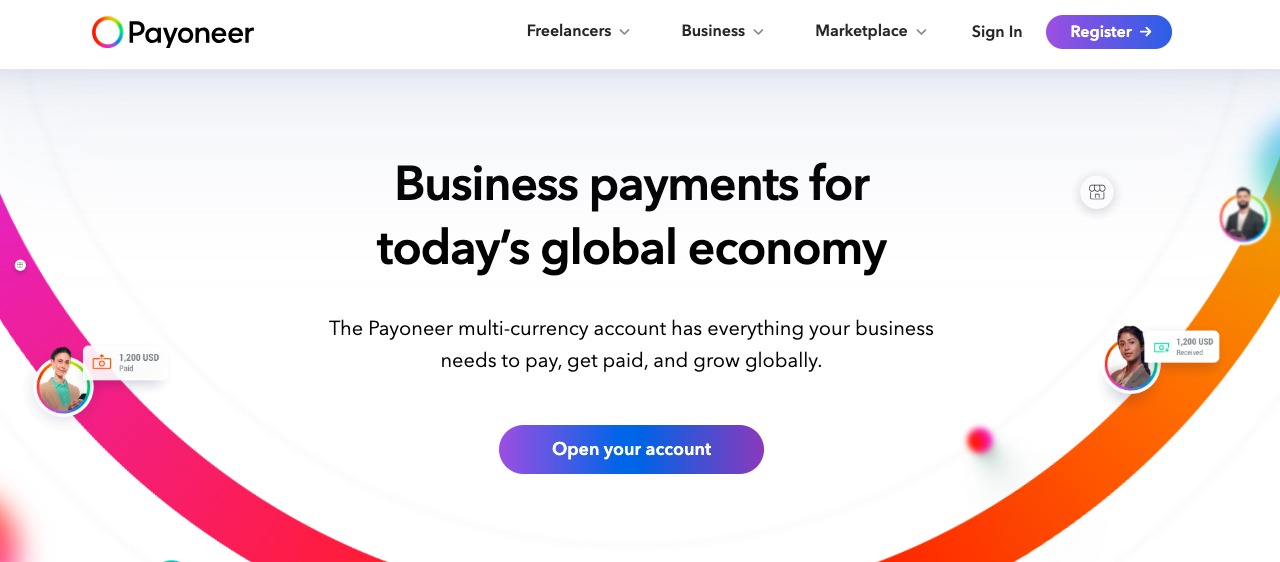

4. Payoneer

Closer to traditional banking, Payoneer targets freelancers and entrepreneurs. Its cards support USD, EUR, and GBP, are accepted in most countries, and are ideal for receiving income from international clients.

Fees are transparent: dollar payments are free, withdrawals cost 2%, and ATM cash withdrawals are 3.5% plus a fixed fee. Card limits are generous — up to $200,000 per day.

Funds can be added via bank transfer or cryptocurrency, and all operations are secured with two-factor authentication. The app makes it easy to track transactions and receive notifications.

Funds can be added via bank transfer or cryptocurrency, and all operations are secured with two-factor authentication. The app makes it easy to track transactions and receive notifications.

Choosing the right card for each purpose

These platforms show how far fintech has come. International payments used to be cumbersome, requiring separate banks, SWIFT codes, long transfers, fees, and unpredictable exchange rates. Now it’s just a few clicks.

A virtual dollar card is no longer just a convenient way to pay for online subscriptions—it symbolizes financial independence. Users no longer depend on banks, countries, or currencies; they control how their money is managed, wherever they are.

To maximize this potential, choose cards for specific purposes. For subscriptions and online services, a simple card without a minimum balance is ideal, which can be instantly blocked after a trial. For travel, a dollar card with clear rates and no hidden fees avoids losses on currency conversions. Freelancers and entrepreneurs need multi-currency options accepting crypto and dollars, while everyday shopping benefits from cards with cashback or rewards. Advertisers benefit from high-limit cards supporting Meta or Google Ads.

When each card serves a clear role, the system works flawlessly. This is the new logic of finance: not one universal card, but an entire ecosystem. Fintech platforms now allow issuing dozens of virtual cards from one interface, with full control over limits, currencies, expiration dates, and purposes. You can create a temporary card for a hotel booking and delete it afterward, without risking data leaks. You can have a dollar card for international purchases and a separate euro card for European expenses.

This is a new level of financial personalization: you don’t adapt to the system—you build it for yourself.

Borderless finance: what’s next

Fintech doesn’t replace traditional bank cards, it enhances them. Virtual cards have achieved what banks could not: removing unnecessary steps and showing that financial freedom isn’t one universal card but a customizable set of tools.

True payment flexibility comes from simple, reliable, and intuitive instruments that together give financial independence and control over money anywhere in the world.

The future of this freedom is even more impressive. Virtual cards will become part of personalized ecosystems, where users can create, combine, and manage dozens of cards for specific purposes. Limits, currencies, expiration dates, and card uses will be fully customizable, with instant integration for crypto and international payments. Instead of adapting to banking products, users will build their financial systems and pay in the currency they choose anywhere on the planet.